The most defining feature of the business plan document when sent out is that it gets read without you, the founder. When an investor, a bank, a potential partner, or a grant committee reads your business plan, you are not there to fill the gaps. You are not there to sense the moment they become confused and step in to clarify, or to read the room when a section lands badly and recover with energy or humour. After it has been sent, the document is doing the entire job, alone, in a room you have never been in, in front of someone whose decision you need.

This means the business plan is not just a record of your thinking, but a performance of your thinking, and like any performance, it communicates more than its explicit content. Everything in it, from the structure and language signal, simply shows how clearly you understand your own business and all of this happens before the investor has formed a conscious opinion about the business itself.

Investors are evaluating whether the person who wrote this document is someone they can trust with money. Your writing is the evidence.

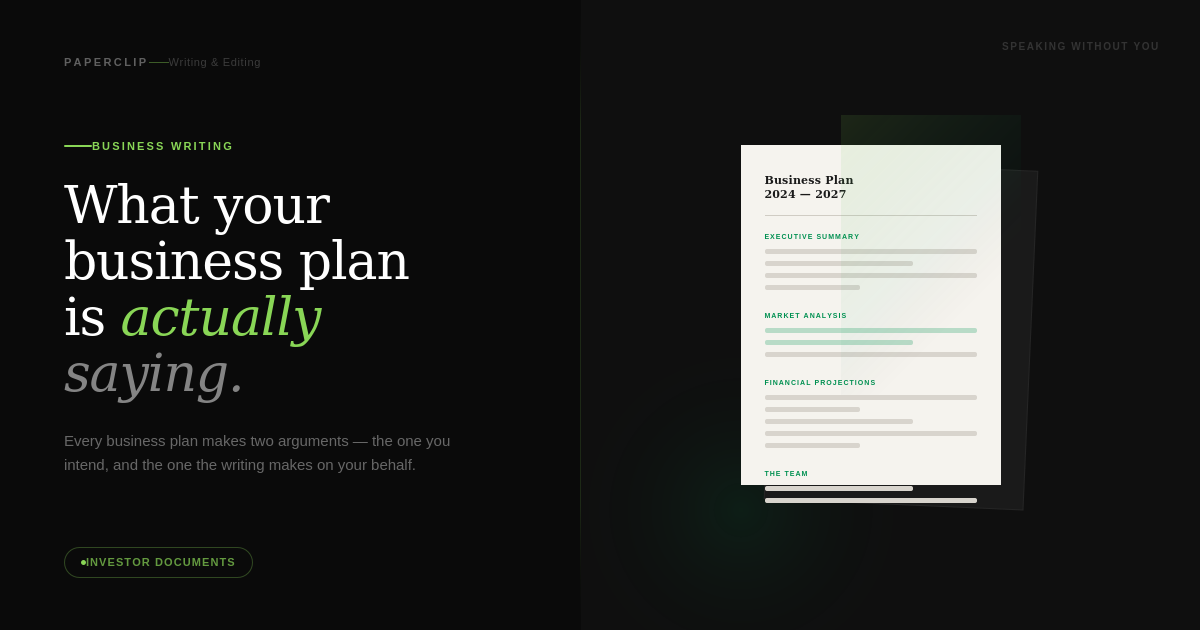

What the executive summary is doing

The executive summary is read first and remembered longest; in fact, for many investors reviewing a high volume of plans, it is the only section that determines whether the rest gets read at all. However, most business plan executive summaries fail at making the reader need to know more.

The most common failure of this section is compression. Founders take their business plan and try to squeeze all of it into two pages, thereby producing a dense, jargon-heavy summary that tells the reader everything and compels them toward nothing. A summary that covers every section of the plan is more of an index than a summary.

An executive summary that works makes one coherent argument: here is the problem, here is why now, here is why us, here is what we need and what it will produce. That is four ideas. They should fit on a page, written in plain English, with enough specificity to be credible and enough clarity to be memorable. Everything else would go into the body of the plan.

The market analysis section: where credibility is made or lost

Nothing signals the quality of a founder's thinking more directly than the market analysis section, and this is because it is the section where the relationship between ambition and evidence is most clearly exposed.

The specific failure mode is the top-down market sizing that produces impressive numbers with no connection to the actual business. "The global logistics market is valued at $8.1 trillion. We are targeting 0.1% of this market, representing an $8.1 billion opportunity." This approach, where you take a large number, apply a small percentage, and then present the result as an opportunity, is immediately recognisable to experienced investors and immediately damaging to credibility. It signals that the founder has not done the work of understanding their actual addressable market.

The alternative is bottom-up market sizing: who specifically will buy this, how many of them there are, what they will pay, and how many we can realistically reach over the period the plan covers. This approach produces smaller numbers, but they are defensible numbers, and a defensible small number is worth infinitely more in an investment conversation than an indefensible large one.

The market analysis section should also address competition honestly, as every business faces competition, including customers doing nothing or solving the problem themselves. A business plan that claims no significant competition does not signal a founder who has not looked carefully enough.

The financial projections: what investors are reading

Financial projections in a business plan are not primarily evaluated for their accuracy. Everyone involved in an investment conversation understands that three-year projections for an early-stage business are, at best, an educated guess. What investors read in the financial projections is the quality of the thinking behind them.

Specifically:

Are the assumptions stated explicitly, or do the numbers appear without explanation?

Are the growth rates plausible given the business's current stage and the market's actual growth rate?

Does the cost structure reflect a genuine understanding of what it takes to operate this business?

Is there a coherent link between the funding being requested and the specific milestones the plan claims it will achieve?

A funding ask of $500,000, followed by projections showing rapid growth, is not a financial argument. The financial section needs to show, specifically, what that $500,000 will be used for, what it will make possible that is not currently possible, and how the plan changes if the funding is not secured in full.

A business plan whose projections include a downside scenario, what happens if customer acquisition costs are higher than projected, or if the sales cycle is longer, signals a founder who is thinking rigorously rather than blindly optimistic. This is more valuable to a sophisticated investor than a single set of aggressive projections.

The language of risk: how you write about uncertainty matters

Every business faces risk, and investors know this. And so, what distinguishes a founder who can be trusted with capital from one who cannot is the quality of their engagement with risks.

A business plan that tries to catalogue every possible risk misses the point. This section should do one thing well, which is to show that the founding team understands the risks most relevant to the business, has a realistic view of their likelihood and impact, and as well has a credible plan to manage those it can control.

Here, language matters as much as substance. “We do not anticipate significant regulatory headwinds” is very different from “Current regulatory trends in this sector present a manageable risk, and we have engaged external counsel to monitor changes that may affect our operating model.” One brushes the issue aside; the other shows active engagement, and this difference is one Investors notice.

What the writing says about the team

In the early stages of a business, investors often say they are backing the team as much as the idea. The business plan is where the team makes its case, not just in a team biography section but throughout the document.

A business plan that is clearly written signals a team that thinks clearly, whilst a plan that is vague about how the business model works, or that uses complexity as a substitute for explanation, signals a team that either does not fully understand its own business or does not trust the reader to follow a clear argument.

The team section itself should go beyond credentials and roles and should answer the question an investor is asking: why is this specific combination of people the right one to execute this specific plan? That question is answered not by listing qualifications but by connecting the team's specific experience to the specific challenges the business will face.

The document as a first impression

A business plan is, among other things, a demonstration of how this organisation communicates. If the plan is well-structured, clearly written, and precisely argued, it suggests that the same qualities will be present in how the business communicates with clients, manages relationships with partners, and reports back to investors after funding is secured.

If the plan is disorganised, imprecise, or written as if the primary goal was length rather than clarity, it suggests the same.

Most founders treat the business plan as a prerequisite to conversation, but the founders who secure funding treat it as a conversation starter. The difference is whether they recognise that the document speaks for them in every room they cannot enter, to every decision-maker they need to persuade.

Write with that in mind.